Make it Zero have developed 10 guiding principles to support the targets. The aim of these is to provide detail and clarity as to what the sector targets mean by providing a succinct and readily understandable summary of the targets and thus ensure signatories set robust targets and follow best practice.

Boundary and Baseline

1. Use the company boundary as used for financial accounting.

The company boundary defines the scope within which your company operates, establishing the limits for responsibilities, control and operations. As such this boundary should also be applied to emissions to reflect what you will have the ability to decarbonise. The boundary for financial accounting is robust and readily understood by your company and so should also be used for carbon accounting.

2. Use a year with accurate data reflective of current operations for the baseline for both the near term and long-term targets, aligning to any applicable reporting requirements for baseline selection.

Baseline emissions are those associated with your company’s operations for a calendar or financial year. This is the starting point against which your target is set, and then comparisons of the emissions reductions achieved are made. It should represent your whole company within the agreed boundary and draw from as accurate data as possible and be reflective of current operations, so as to facilitate fair comparisons in future. The same baseline year should be used for the near and long-term targets. It is worth noting that some reporting requirements, such as SBTi and CSRD have restrictions on how old a baseline can be and so these should be adhered to if you are complying with these schemes.

3. Include all greenhouse gas emissions resulting from the companies' activities, as defined by the GHG Protocol Corporate Standard

Greenhouse gas (GHG) emissions are gases that when released into the atmosphere contribute to global warming. The predominant of these is carbon dioxide (CO2), and so the other gases are often expressed in their carbon dioxide equivalent (CO2e) and included in carbon emission calculations. Your activities (such as energy use, transport, waste disposal) will have emissions associated with them, which can be calculated using the emission factors for that activity. All activities within the company boundary should be included in the emission calculations, though there can be some exclusions made of immaterial emissions sources where it is not efficient or practical to regularly measure them. The primary guidance for emissions calculations is the GHG Protocol Corporate Standard and this should be adhered to.

4. Use the same approach for scope 2 emissions in the base year and target year (market based or location based).

Scope 2 (Indirect emissions from purchased energy) are GHG emissions from the generation of purchased electricity, steam, heating, and cooling consumed by the company. These emissions occur at the facility where the energy is generated, not at the company using the energy. There are two means to calculating these: market based, where an emission factor specific to the energy contract obtained from your supplier is used, or location based, where an average factor for the local, regional or national grid is used. Either approach is acceptable, but the same approach should be used for the baseline and target year. If you choose a market-based approach for your target, which enables you to account for the emissions reduction benefit of sourcing lower carbon electricity via the market, the GHG Protocol states that you should still also publish location-based scope 2 figures alongside it, each year, for reasons of transparency.

Targets and Trajectories

5. Cover at least 95% of scope 1 & 2 and 67% of scope 3 emissions through the corporate target and supplier engagement target, making any necessary allowances for SMEs.

Scope 1 (Direct emissions) are GHG emissions from sources that are owned or controlled by the company, such as emissions from company-owned vehicles or on-site fuel combustion and Scope 2 (Indirect emissions from purchased energy) are GHG emissions from the generation of purchased electricity, steam, heating, and cooling consumed by the company. At least 95% of these (as per your baseline year) should be covered by your corporate target.

Scope 3 emissions (Other indirect emissions) are other indirect emissions not covered in Scope 2 that occur in the value chain of the company, both upstream and downstream. At least 67% of these (as per your baseline year) should be covered between your corporate target and supplier engagement target. It should be noted that small and medium-sized enterprises (SMEs) may find setting and achieving decarbonisation targets more challenging and so allowances need to be made for them, such as initially focusing targets on larger suppliers.

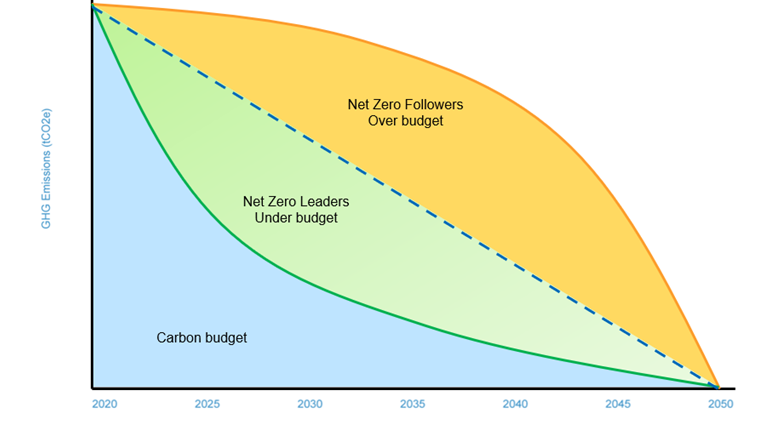

6. Be on or below the decarbonization trajectory required to keep global temperature increase to 1.5°C compared to pre-industrial temperatures for scope 1 and 2.

In order to keep the global temperature, increase to 1.5°C compared to pre-industrial temperatures (1850 to 1900) a defined decarbonisation trajectory is required (as defined by the Paris agreement). This is because when greenhouse gas emissions are released into the atmosphere they can remain there for thousands of years and so the cumulative emissions (carbon budget) released between the baseline year and target endpoint also need to be considered and managed, as well as those at the endpoint year. As such the emissions trajectories companies follow to achieve their target should be on or below this trajectory. The figure below provides an indicative illustration of how a company may achieve its endpoint target of net zero by 2050 but have exceeded its carbon budget by having been above the trajectory.

7. Be on or below the decarbonization trajectory required to keep global temperature increase well-below 2°C compared to pre-industrial temperature for near term scope 3.

As with scope 1 & 2 in order to limit the global temperature increase the decarbonisation trajectory as defined by the 2015 Paris agreement needs to be followed. To reflect the more challenging nature of scope 3 the trajectory needed to keep the global temperature increase to well-below 2°C compared to pre-industrial temperature may be followed, though the more stringent 1.5°C trajectory is still recommended if you feel it is feasible for your business.

The Science Based Target Initiative defines the well-below 2°C trajectory as a linear reduction rate of at least 2.5% a year compared to your baseline

8. Use eligible intensity metrics approaches.

There are two main types of emissions reduction targets, absolute and intensity based. Absolute targets are based on the total emissions in the baseline and target year and the total emission reductions between the two.

For scope 3 intensity-based targets may be used. These are based on emissions per a physical or economic metric. These can be beneficial in reflecting GHG performance independent of business growth or decline, but do not necessarily lead to reductions in absolute emissions in cases where the output increases. Physical intensity metrics must be a representative measure of your company’s activity, such as employee headcount, retail area, units sold or production input or output in tonnes. Possible economic intensity metrics include revenue and Gross Value Added.

Reducing emissions and reporting

9. Not count carbon credits or avoided emissions as emission reductions (only for neutralizing the residual emissions through measures that remove emissions from the atmosphere)

Carbon credits, also known as carbon offsets, are traded permits that represent reduced or avoided emissions that occur outside your organisation, such as forest conservation or funding renewable energy developments in developing countries. They can be purchased by businesses to offset an equivalent quantity of emissions to achieve a status of “carbon neutral”.

However, international standards around carbon offsets are in a state of flux, with the quality and longevity of their carbon savings uncertain. Your target should solely drive genuine emissions reductions in your own value chain. As such, offsets should not be counted as emission reduction measures. You may, however, still choose to purchase carbon offsets of an acceptable standard as an additional environmental measure.

While offsets cannot be used to reduce emissions to meet reduction targets, there may be a requirement to use emission removal projects that extract carbon from the atmosphere to achieve a net zero target, such as permanent tree planting or direct air capture and storage. These could take place in your own value chain, or they could also be funded via carbon credits.

Avoided emissions are the emissions that are prevented by using a product or service that you sell, compared to a higher emission alternative product or scenario. They are sometimes referred to as “Scope 4”. For example, you may sell air source heat pumps to replace natural gas boilers in customers’ homes, helping them reduce their own emissions.

The theoretical emission savings from these falls outside your company emissions boundary and so should not be included as emissions reductions in scope 1, 2 or 3. Note that the benefits from providing lower carbon products or services than previously, would already potentially get captured as emission reductions specifically in scope 3 category 11 use of sold products

10. Publicly state targets and report progress against them on an annual basis

The targets should be stated in a publicly accessible place (such as annual financial report, sustainability report or your website) and progress against them reported on annual including as a minimum the baseline emissions, current year’s emissions, percentage change between the two and percentage change that would be required to meet the target. It would be recommendable to include an explanation of the performance against the target.